This article was written and produced by Futuro Financial Services

The Russia / Ukraine conflict is evolving at a rapid pace with plenty of propaganda and

misinformation doing the rounds along with vested interests and important historical

contexts missing.

Putting that aside, any war / conflict / invasion is a terrible thing to see, and our thoughts

and prayers are with those affected by the conflict.

What we know so far, in what is a very fluid situation, is that Russian troops have moved

into Ukraine from the north, east, and south. It also appears that there’s been no official use

of NATO or allied troops yet.

What we still don’t know are the exact motives for doing so, what the Russians hope to

achieve, and how long they plan to remain in Ukraine. We can guess or speculate, but that

won’t help the situation, and we can confirm that many are guessing and speculating.

What we can and have been focusing on is the economic and financial market implications

of the conflict. These include:

- Sanctions

- Risk sentiment

- Inflation and central banks

Before we get into the details on some of these, it’s worth noting that geopolitical events

rarely have a lasting impact on markets. For example, if you look at the US equity market

(S&P 500) returns and geopolitical events since 1970, the average returns are as follows:

1 week – up 0.1%

1 month – up 0.2%

1 quarter – up 3.6%

1 year – up 9.6%

Coming back to areas of focus, Russia has been hit with plenty of actual and proposed

sanctions from the West, which is to be expected. These sanctions have the ultimate aim of

trying to stop further conflict by:

- Crippling Russia economically

- Causing politically pressure / instability to weaken or topple Putin

There’s a strategy of sorts behind how and when you apply sanctions. Go too hard early and

you embolden the aggressor to act more aggressively; go too soft early and you let your

aggressor know that you’re not serious or that you don’t want to harm yourself in the

process (e.g., oil and gas). Sanctions thus far have been weak to reasonable, so there’s

plenty of room to ramp these up if needed.

Risk sentiment is clearly negative at present with investors looking for safety in assets like

cash, government bonds, quality equities, gold, and safe-haven currencies such as the

Japanese Yen, Swiss Franc, and the US dollar. However, this negative sentiment is polluted

by the negative sentiment that already existed before the conflict owing to concerns

regarding high inflation and how central banks are likely to fight inflation. That is, we don’t

know how much of the current negative sentiment is due to the conflict versus the concerns

about central bank rate rises. Right now, we’d say that the conflict is responsible for the

negative sentiment at the surface, but the underlying driver of the negative sentiment

remains inflation.

Following on from that, and perversely so, the conflict has given central banks the breathing

room they so desperately needed to slow and calm market sentiment regarding the amount of

rate rises that were likely this year. In stark contrast to that, the conflict could actually exacerbate

already high levels of inflation through higher oil and gas prices and further supply shortages, thus

exerting additional pressure on central banks.

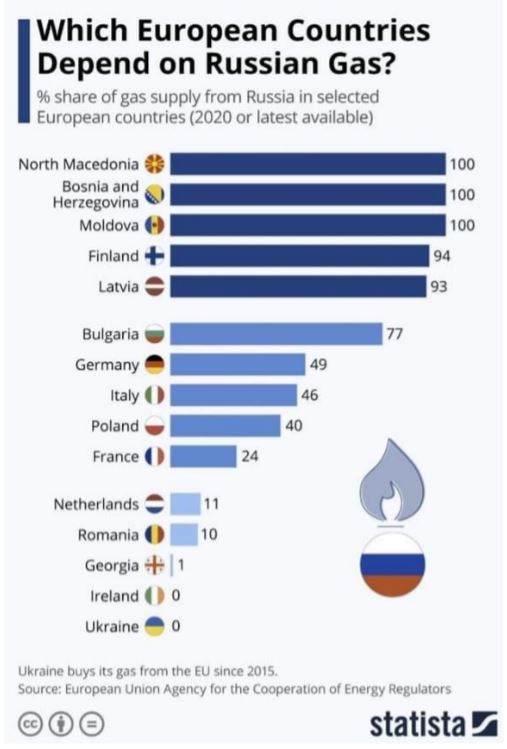

One thing we are watching closely is oil and gas prices, along with oil and gas demand and

supply, and how that might impact consumption, business investment and earnings, and

political manoeuvring especially in the lead up to elections where energy security is likely to

be a hot topic.

KEY TAKEOUT’S ARE AS FOLLOWS

- Our thoughts and prayers go out to the people caught up in the conflict

- Geopolitical tensions rarely have a lasting impact on markets, since they rarely have a

lasting impact on the business cycle - We think a resolution to the conflict is likely, but have no guidance on the timeframe

- Our base case remains that central banks don’t need to raise rates aggressively from

here, but that rates should be higher than they are currently - The negative sentiment since the beginning of the year is more an opportunity than it is

a risk.

As such, we don’t believe significant portfolio changes are required given the fluidity of the

situation and given portfolios remain well positioned. But we remain very watchful of the

prevailing news, data, and market conditions. Dollar cost averaging and portfolio

rebalancing might be worth exploring further at this juncture.

This article was written and produced by Futuro Financial Services

Recent Comments